In America, loans serve as a critical financial tool, allowing individuals like you to achieve both immediate needs and long-term goals. Whether it’s the dream of owning a home, the pursuit of higher education, or the desire to start a business, loans provide the necessary financial support to make these aspirations a reality. They function as a bridge between your current financial position and your future ambitions, offering the leverage needed to make significant life changes that might otherwise be unattainable.

However, using loans effectively requires a nuanced understanding of how they work, the various types available, and the responsibilities that come with borrowing. By grasping the complexities of loans, you can strategically use them to your advantage, building wealth and securing a more stable financial future.

Exploring the Different Types of Loans

In the United States, loans come in various forms, each tailored to meet specific financial needs. Mortgage loans, for example, are designed for those looking to purchase real estate. These loans are typically long-term commitments, with repayment periods extending up to 30 years. The stability of mortgage loans makes them a popular choice for homeowners looking to build equity over time.

Auto loans, on the other hand, are specifically intended for purchasing vehicles. These loans generally have shorter repayment terms, often ranging from three to seven years. The shorter duration reflects the depreciating nature of vehicles, ensuring that your loan term aligns with the lifespan of the car.

For those pursuing higher education, student loans offer a lifeline to cover tuition and related expenses. These loans often come with favorable interest rates and flexible repayment terms, recognizing the long-term investment in your future earning potential.

Personal loans stand out for their versatility. They can be used for a wide range of purposes, from consolidating debt to funding home improvements or covering unexpected expenses. The flexibility of personal loans makes them a convenient option for managing various financial needs.

Lastly, business loans provide essential capital for entrepreneurs. Whether you’re starting a new venture or expanding an existing one, business loans offer the financial support needed to grow your enterprise. The right business loan can be a catalyst for success, providing the resources necessary to scale operations, hire employees, and increase profitability.

Understanding Interest Rates and Loan Terms

Interest rates are a critical factor in determining the cost of borrowing. They represent the price you pay for the privilege of using someone else’s money. The rate you receive depends on several factors, including your credit score, the type of loan, and prevailing market conditions. Fixed interest rates offer the predictability of consistent monthly payments, making them an attractive option for those who prefer stability. However, variable interest rates, which can fluctuate over time, may initially offer lower payments but carry the risk of increasing costs.

The term of your loan, or the length of time you have to repay it, also plays a significant role in the overall cost. Longer loan terms typically result in lower monthly payments, making them more affordable in the short term. However, the trade-off is higher total interest costs over the life of the loan. Conversely, shorter loan terms require higher monthly payments but result in lower overall interest expenses, allowing you to save money in the long run.

When considering a loan, it’s essential to weigh both the interest rate and the term. For instance, a 30-year mortgage with a low fixed rate might seem appealing due to its manageable monthly payments, but a 15-year mortgage could save you thousands of dollars in interest, despite the higher payments.

The Influence of Credit Scores

Your credit score is a crucial determinant of your loan eligibility and the interest rates you’ll be offered. A high credit score signals to lenders that you’re a responsible borrower, which can result in more favorable loan terms, including lower interest rates. In contrast, a lower credit score may limit your borrowing options and lead to higher rates, increasing the cost of your loan.

Maintaining a good credit score involves consistently paying your bills on time, keeping your credit utilization low, and avoiding excessive credit inquiries. If your score isn’t where you’d like it to be, there are steps you can take to improve it. Paying down existing debt, correcting any errors on your credit report, and limiting new credit applications can all help boost your score before applying for a loan.

The Benefits of Using Loans Wisely

When managed responsibly, loans can be a powerful tool for achieving financial freedom. They enable you to make substantial investments in your future, such as purchasing a home, advancing your education, or starting a business. These investments often lead to increased income, wealth accumulation, and a more secure financial future.

For example, taking out a mortgage to buy a home can be a strategic financial decision, as real estate tends to appreciate over time. This appreciation builds equity, which can be leveraged for further investments or provide a financial cushion in times of need. Similarly, student loans, when used to gain the skills and qualifications needed for a higher-paying career, can offer a significant return on investment. Business loans provide the capital necessary to turn entrepreneurial ideas into thriving enterprises, with the potential for substantial financial rewards.

However, the key to benefiting from loans lies in borrowing within your means and fully understanding the terms of your loan. By doing so, you can use loans to build wealth rather than falling into a cycle of debt.

Building Wealth Through Real Estate

Real estate is one of the most reliable ways to build wealth in America, and mortgages make property ownership accessible to many. As property values typically increase over time, homeowners can build significant equity, which can be tapped into for other financial ventures. Moreover, owning a home often comes with tax benefits, such as deductions on mortgage interest and property taxes, which can reduce your overall tax burden.

These advantages make real estate an attractive option for those looking to build long-term wealth. However, it’s essential to approach homeownership with a clear understanding of the responsibilities involved, including mortgage payments, property maintenance, and the potential risks of market fluctuations.

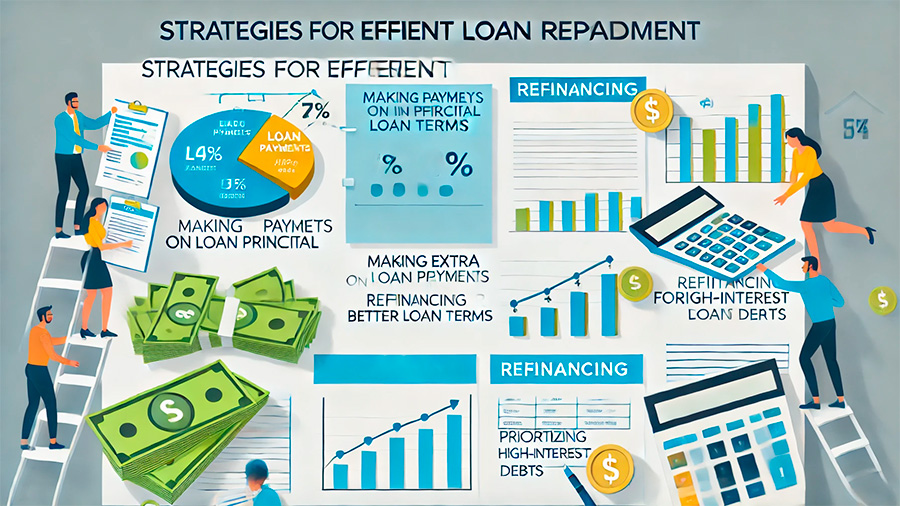

Strategies for Efficient Loan Repayment

Effective loan repayment strategies can save you money and shorten the time it takes to pay off your debt. One approach is to make extra payments on your loan’s principal. By doing so, you reduce the overall amount on which interest is calculated, leading to significant savings over the life of the loan. Even small additional payments can make a noticeable difference in the total interest paid.

Refinancing is another strategy to consider. This involves taking out a new loan with better terms to pay off an existing loan. Refinancing can lower your interest rate, reduce your monthly payments, or shorten your loan term, depending on your financial goals. It’s a strategy that can provide relief if your financial situation has improved since you first took out the loan.

Prioritizing your debts is also crucial. Focus on paying off high-interest loans first, as this approach minimizes the amount of interest you pay overall and helps you become debt-free faster. By strategically managing your debt repayment, you can reduce financial stress and free up resources for other financial goals.

Utilizing Debt Consolidation

If you find yourself managing multiple loans or credit card debts, debt consolidation can offer a practical solution. This process involves taking out a new loan to pay off your existing debts, leaving you with just one monthly payment to manage. Consolidation simplifies your finances and can potentially reduce your interest rates if the new loan offers better terms.

Debt consolidation can be particularly beneficial if you’re struggling to keep track of multiple payments or if your existing debts have high interest rates. However, it’s essential to avoid accumulating new debt after consolidating, as this can lead to an even more challenging financial situation.

Conclusion

Loans, when used wisely, are a valuable tool in unlocking financial freedom in America. By understanding the various types of loans available, the impact of interest rates and loan terms, and employing effective repayment strategies, you can leverage loans to achieve your financial goals and build lasting wealth. While loans provide opportunities to make significant investments in your future, it’s crucial to approach borrowing with a clear plan and a thorough understanding of the responsibilities involved. With careful management, loans can serve as a powerful ally in your journey toward financial independence and security.